$VIAC: ViacomCBS Executive Summary

Is $VIAC a buy the dip opportunity?

Company Overview:

ViacomCBS is a multinational media conglomerate that owns popular media brands such as Nickelodeon, MTV, BET, Comedy Central, Showtime, Paramount Pictures as well as distribution rights to major sporting events like March Madness, The Masters, SEC college football, and American Football Conference (AFC) games. Viacom and CBS, two legacy media powerhouses, merged in 2019 to created ViacomCBS with the rationale being that the combined company would be able to compete more effectively in the growing streaming market than as stand-alone players. Bob Bakish was appointed the CEO of the newly combined by recommendation from Shari Redstone, Chairman, after serving three years as CEO of Viacom and twenty-two years being a media executive.

Bob Bakish began his career at Viacom primarily in charge of growing the MTV brand both domestically and internationally. In 2011, following the success of MTV’s international expansion Bakish was promoted to become the CEO of Viacom International Media Networks (VIMN) focusing on the international growth of all Viacom brands. During his tenure, VIMN was Viacom’s most successful division with the unit’s revenue more than doubling and demonstrating strong growth in key markets like Europe, India, and Latin America. Afterward, Bob Bakish was named CEO of Viacom in 2016 with the tall task of turning the company around and returning the advertisement business (Viacom’s largest revenue stream) to growth while streaming was disrupting the entire entertainment industry. He was ultimately able to succeed in getting the advertisement business back to double-digit growth QoQ and improve the overall profitability by fully integrating the company with one large production studio, one licensing arm, and a combined advertisement business to leverage economies of scale. Bob Bakish’s many years of industry experience and track record of delivering is one of the reasons I am bullish that ViacomCBS will be successful as they fully integrate both companies and transition to becoming a major streaming player.

Financial Snapshot:

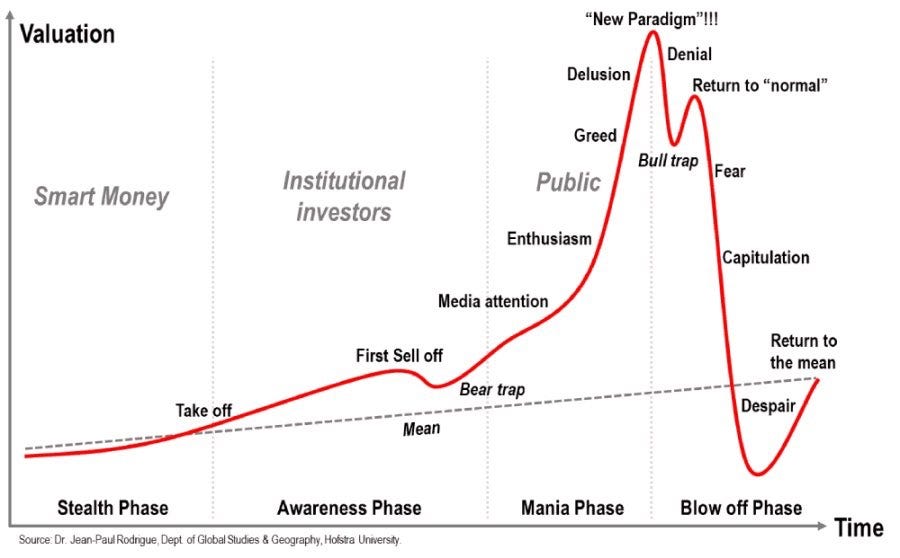

The stock price for $VIAC has had quite the roller coaster over the last year and especially over the last three months with the aftermath of Archegos Capital’s margin call. $VIAC was trading at $100 on March 22nd and currently (May 5th) is trading in the $39s. The image below is a diagram from Dr. Jean-Paul Rodrigue displaying the different market phases for assets. Typically there will be a small rise followed by a rapid rise and then capitulation before returning to steady growth.

The stock chart of $VIAC over the last 6 months is almost identical to Rodrigue’s diagram and with Q1 earnings being released on 5/6 plus a new summer content slate $VIAC could be exiting the blow-off phase. $VIAC is trading at a significant discount when compared to its peers in the communication and streaming sectors that trade at an average above 20x P/E. The image above shows the end of the year 2020 financials for both Netflix (left) and ViacomCBS (right).

In a year where cord-cutting was accelerated, movie theatres were mostly closed, and marquee sports events like March Madness were canceled...ViacomCBS was still able to generate 2.3 billion dollars in profit, not including the 2.4% dividend they continued to pay shareholders. Netflix enjoys a much higher valuation multiple, like many tech companies, as the market is betting on Netflix to keep driving growth and doesn’t place the same confidence in ViacomCBS. The bearish case for $VIAC is that developing hit programs for streaming is difficult and that streaming is a different game than cable. However, in the next section, I am going to look at how $VIAC has already proved they can succeed in streaming and why their unique strategy for streaming will succeed.

Differentiated Streaming Strategy:

$VIAC believes in building a direct-to-consumer (DTC) ecosystem of streaming from Pluto TV (FAST) to Paramount+ (AVOD) to Showtime/BET+ (SVOD). Netflix, Disney+, and even HBO Max have been spending billions of dollars all fighting over the same slice of streaming, premium ad-free subscriptions for young adults/millennials, in reality, that’s just one segment of the entire streaming market. Pluto TV can attract people who don’t want to pay for streaming right now and eventually convert them to become subscribers for one of their products. Viacom acquired Pluto TV in 2019 for $340 million with the belief their library of content would help accelerate Pluto TV’s growth and the company has been largely correct. By the end of 2020, Pluto TV had become the largest free streaming service with over 42 million monthly active users (MAU) and is projected to do over $1 billion in advertising revenue by 2022.

A common criticism of the company entering streaming is that they keep licensing out their top content like Yellowstone and will fail to have compelling content to attract subscribers. ViacomCBS plans to remain a major player in the licensing market with content being even more valuable in a streaming world. The launch of Disney+, HBO Max, Peacock have all focused on making their content exclusive to their platforms to accelerate subscriber growth, but have effectively cannibalized their licensing businesses. The lack of supply caused by exclusivity and growing demand from streaming services needing hit content to stand out has caused the licensing business to become highly lucrative. $VIAC views the licensing business as a growth engine both financially and strategically to expand their current footprint.

$VIAC’s Content Decision Framework:

Financials: How much could this piece of content get as a licensing agreement? What is the opportunity of cost keeping it exclusive for $VIAC?

Streaming: How does an exclusive piece of content drive growth via our streaming offerings? How can this drive the growth of other products like amusement parks, merchandise, gaming, Pluto TV?

Partnerships: How does doing a partnership impact the studio or pipeline of creative opportunities (spin-offs)? How does doing a partnership impact distribution and global reach?

Double Dipping:

The framework above shows the key factors ViacomCBS takes into account in their decision making, let’s use some real world examples to evaluate the framework. ViacomCBS made the decision to license out the U.S. streaming rights of South Park via bidding war to HBO Max for above $500 million. South Park being exclusive to Paramount+ wouldn’t have even brought in $100 million in additional streaming revenue, HBO Max gives the show a reach to different audience plus the deal will eventually expire and be added to Paramount+ in the future converting hardcore fans.

In 2019, Nickelodeon striked a production deal worth over $200 million with Netflix and on February 8th, 2021 the first two seasons of Icarly were added to Netflix. Over the following months Icarly became one of the most watched shows on Netflix. Many of Netflix’s 200 million subscribers began binging the show with even more at least seeing the show engrained to Netflix’s Top 10 Most Watched list. A critique is that keeping a show like Icarly exclusive could have attracted more subscribers to Paramount+ as it clearly was a popular show people wanted to watch, but ViacomCBS is using Netflix as a marketing tool. An Icarly reboot is going to premiere exclusively on Paramount+ later this year and thanks to Netflix the franchise hasn’t been this popular since the show was airing in 2012. The same strategy was applied to Avatar: The Last Airbender, a mainstay in Netflix’s Top 10 Most Watched for 2020, where the franchise has never been more popular with a new series and feature films now being produced exclusively for Paramount+. Amazon Prime Video, now over 150 million subscribers, has been paying for the exclusive streaming rights of SpongeBob SquarePants for years, and starting next month ViacomCBS is launching a spin-off exclusively for Paramount+. All three of these shows could have been kept exclusive to Paramount+, but ViacomCBS realized that they would only reach their 30 million existing subscribers and that licensing can be an effective brand-building strategy, especially for long-term growth